Summary

A practical legal guide to settlement valuation, claim timelines, and evidence preservation in U.S. car accident cases. Learn how to maximize your claim value.

Quick Legal Answer: What this guide covers

A practical legal guide to settlement valuation, claim timelines, and evidence preservation in U.S. car accident cases. Learn how to maximize your claim value.

Quick Legal Answer: Core legal focus

This guide focuses on car accident attorney settlement value within car accident guides and the evidence, timelines, and standards typically evaluated under U.S. law.

Quick Legal Answer: When to verify with counsel

Because statutes and rules vary by state, confirm the specifics for your jurisdiction with a qualified attorney or official government resources.

Key Takeaways

- Understand the core rules and evidence standards tied to car accident attorney settlement value.

- Track deadlines and procedural steps that shape recovery options.

- Document medical records, liability proof, and insurance communications early.

- Compare settlement posture with litigation risk based on the case record.

Car Accident Attorney: Settlement Value, Timeline & Evidence Guide

car accident attorney settlement value

Settlement value in a U.S. car accident case is built from records. car accident attorney settlement value depends on proof of liability, documented damages, and a clear claim timeline tied to treatment milestones and insurer response cycles. A settlement-ready file prioritizes evidence preservation and disciplined settlement negotiation for a fair car accident settlement. It also connects the auto accident claim narrative to collision liability, personal injury damages, and any insurance bad faith issues. Strong files document a pain and suffering claim, medical bills recovery, and lost wages claim, while accounting for comparative fault rules, a persuasive demand package, and the practical ceiling set by policy limits. This guide explains how value is calculated, why timelines stretch, and which evidence is most persuasive under U.S. tort law.

This overview explains how car accident attorney settlement value considerations shape evidence, liability, and recovery planning.

Car accident claims are governed by state negligence rules, but the structure of the record is consistent nationwide. Insurers evaluate liability, then quantify damages using proof of loss, medical causation, and policy limits. Courts apply civil procedure rules and evidence standards if a lawsuit is filed. This article is a step-by-step reference for building a settlement-ready file, with emphasis on claim timeline control, evidence preservation, settlement negotiation, demand letter strength, insurance adjuster interaction, comparative fault analysis, and accurate medical records.

To keep your evaluation complete, review each of these concepts: police report accuracy, wage loss documentation, property damage records, pain and suffering support, treatment gaps and continuity, liability investigation steps, medical lien impact, case manager communication, demand package organization, legal strategy alignment, and trial experience readiness. These secondary keywords are used in their practical context throughout the guide.

Key Definitions and Practical Meaning

Understanding core terms will help you read your claim documents and communicate clearly with adjusters and counsel.

Key Definitions

- Liability: Who is legally responsible; documented in the police report, witness statements, and scene evidence.

- Damages: Losses caused by the crash; reflected in medical bills, wage records, and property damage documentation.

- Policy limits: The maximum insurance payout; shown on the declarations page and confirmed in coverage correspondence.

- Comparative fault: Shared responsibility; evaluated in adjuster analysis and, if litigated, jury instructions.

- Causation: The link between crash and injury; supported by medical records and expert opinions.

Legal Framework That Controls Settlement Value

Settlement value comes from state tort law, but the legal mechanics are similar across jurisdictions. The plaintiff must prove duty, breach, causation, and damages. Insurers value claims by testing these elements against the record.

Federal and State Sources That Shape the Record

- Crash reporting and traffic safety standards are coordinated through federal resources like NHTSA.

- State reporting rules, DMV record systems, and citations are state-specific; many states publish reporting standards on DMV or DOT sites.

- If litigation begins, federal procedural concepts are summarized by U.S. Courts, while state rules govern most personal injury cases.

Why Policy Limits Matter More Than People Expect

Settlement value is constrained by the available insurance coverage. Even when damages exceed limits, the practical ceiling often mirrors the policy. Exceptions include umbrella coverage, multiple liable parties, or bad-faith exposure. A sound valuation includes: the at-fault driver’s limits, your UM/UIM coverage, and any commercial or employer coverage tied to the crash.

Evidence That Most Influences Settlement Value

Insurers and juries value objective, time-stamped records over recollections. The most persuasive evidence usually comes from third-party sources.

Evidence Priority List

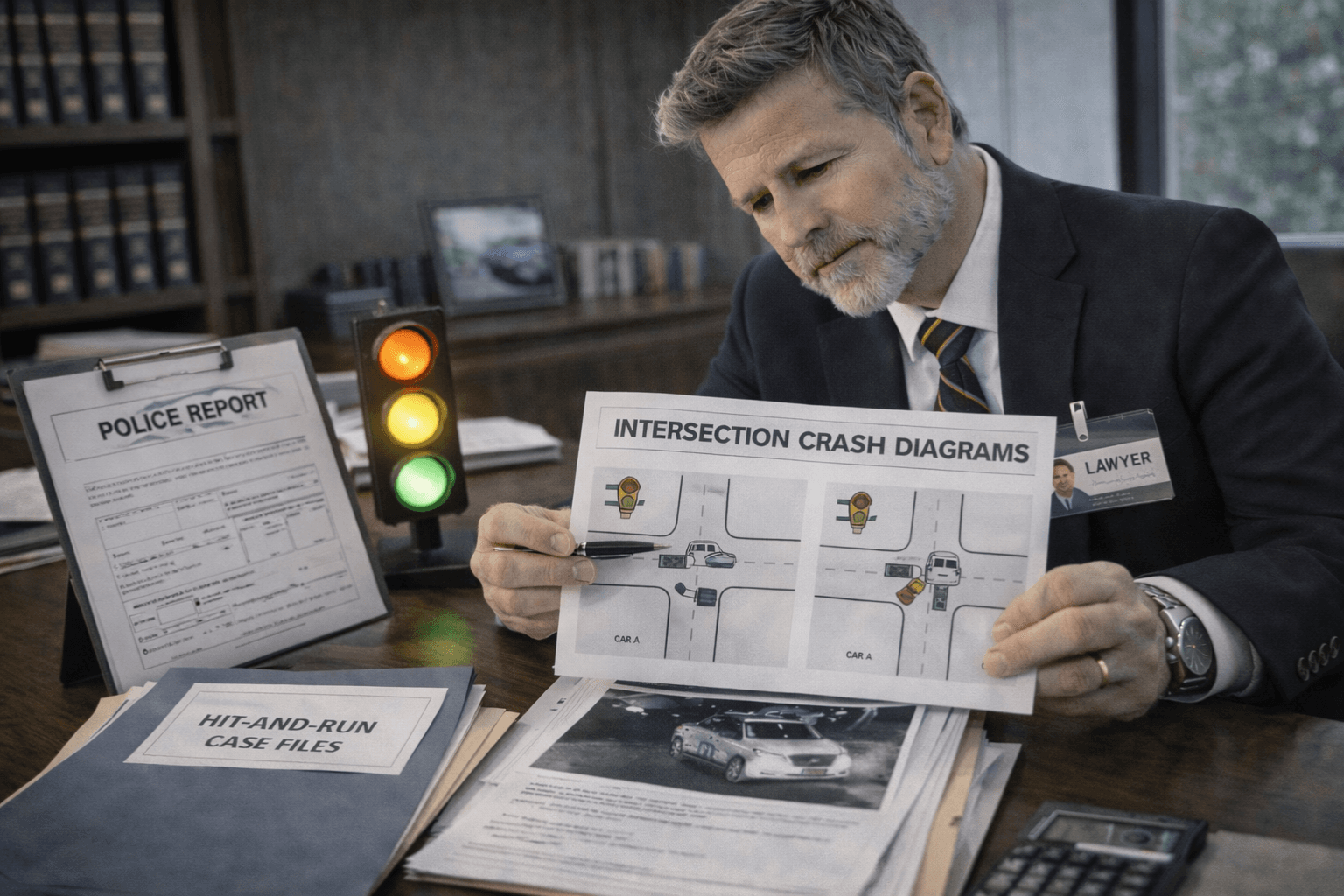

Police report and diagram. Establishes crash location, parties, and potential violations. Photographs and video. Shows vehicle damage, road conditions, and lines of sight. Medical records and billing. Links diagnosis, treatment, and costs to the date of loss. Wage and employment records. Demonstrates time missed and reduced earning capacity. Repair estimates and total-loss valuation. Provides property damage impact and severity context.

Evidence Collection Checklist

- Obtain the crash report number within days of the collision.

- Photograph vehicle damage from multiple angles with time stamps.

- Request EMS or hospital records with full ICD coding.

- Keep a treatment calendar to show continuity of care.

- Save pay stubs and employer letters for wage-loss proof.

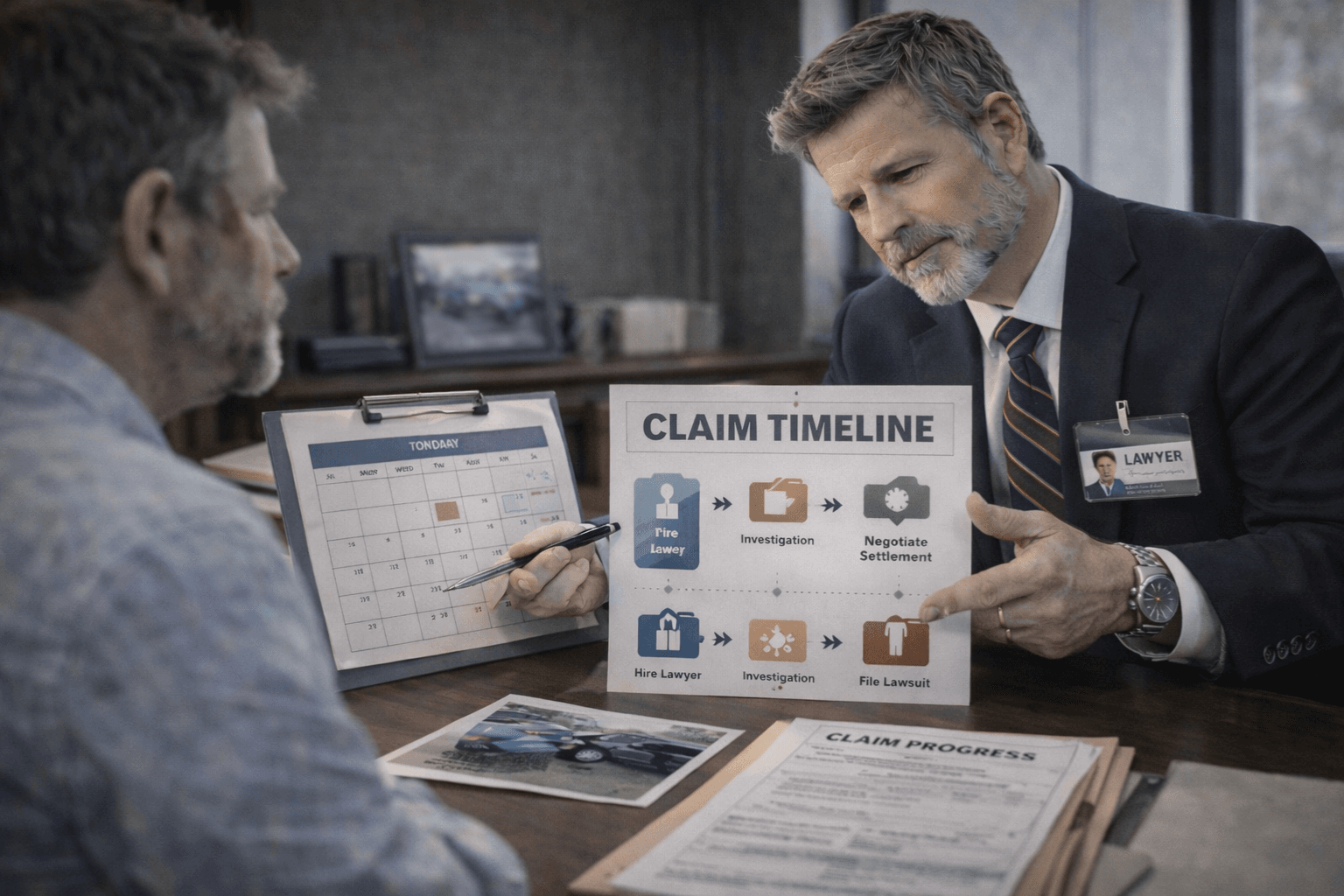

Step-by-Step Claim Timeline (Typical Path)

Claims move faster when documentation is complete. The steps below reflect common practice across states.

Step 1: Immediate Response (Days 0-7)

- Secure the crash report and towing records.

- Get medical evaluation even for soft-tissue complaints.

- Preserve physical evidence, including a damaged helmet or child seat.

Step 2: Early Documentation (Weeks 1-4)

- Request all medical records and itemized bills.

- Photograph healing progression for visible injuries.

- Track out-of-pocket costs such as prescriptions and transportation.

Step 3: Stabilization and Valuation (Months 1-6)

- Reach a stable medical status or documented prognosis.

- Compile a damages package with totals and supporting records.

- Consider future care needs when supported by a provider statement.

Step 4: Demand and Negotiation (Months 3-12)

- Submit a demand letter with organized exhibits.

- Expect the insurer to request additional records or IME scheduling.

- Adjusters typically respond with a counteroffer and rationale.

Step 5: Litigation if Needed (Months 6-24+)

- If negotiation fails, a lawsuit triggers formal discovery.

- Depositions, expert reports, and motion practice shape value.

- Many cases still resolve before trial when evidence aligns.

How Settlement Value Is Calculated in Practice

Most carriers use a valuation model that combines special damages (economic loss) and general damages (pain and suffering), then adjusts for liability and limits. The practical formula is:

Economic loss (medical + wage + property + out-of-pocket) Non-economic loss (function, pain, and daily impact) Comparative fault adjustment Policy limit cap

Economic Loss Components

- Past medical bills

- Projected future care (if supported by medical opinion)

- Lost wages and reduced earning capacity

- Property damage and replacement costs

- Necessary transportation and care assistance

How Adjusters Review the Evidence Packet

Adjusters compare the demand package against objective records. A strong packet is organized, indexed, and easy to verify. Inconsistent dates, missing billing summaries, or unclear treatment notes slow evaluation and reduce leverage.

Demand Package Structure (Best Practice)

- Cover letter summarizing liability and damages

- Liability section with crash report, photos, and citations

- Medical chronology with key records and billing totals

- Wage loss documentation and employer letters

- Property damage evidence and valuation support

Medical Documentation and Causation

Causation connects the crash to the injury. The strongest records include objective findings, diagnostic imaging, and consistent clinical notes that describe symptoms and functional limitations. A provider’s narrative report can be helpful when the injury is complex or involves future care.

Practical Causation Notes

Ensure early records reference the crash date and mechanism of injury. Later records should reflect continuity of symptoms and treatment progression.

How Treatment Gaps Affect Value

Treatment gaps are common but can create questions about whether the injury was caused by the crash. When a gap exists, include documentation explaining the delay, such as appointment availability, travel, or insurance processing.

Negotiation Workflow and Common Responses

Typical Adjuster Responses

- Request for additional records or bills

- Dispute over diagnosis or causation

- Comparative fault allegations

- Policy limit confirmation or limits demand request

How to Respond to Common Pushback

- Provide supplemental records with a short explanation

- Address causation disputes with objective findings

- Use the crash report and witness statements to counter fault claims

- Confirm policy limits and document any coverage gaps

Evidence Timing: What to Request and When

Early-Stage Requests (Days 0-30)

- Crash report and citations

- Scene photos or traffic camera footage

- Vehicle inspection and repair estimates

Mid-Stage Requests (Weeks 4-12)

- Complete medical records and itemized bills

- Wage loss documentation

- Specialist referrals and imaging reports

Late-Stage Requests (After Treatment Stabilizes)

- Future care estimates

- Functional capacity evaluations

- Final billing summaries

Evidence Strength vs Settlement Speed

Use these scenarios to compare risk and timing without relying on a one-size approach.

Strong liability with complete records tends to move faster with lower risk; an early demand is often appropriate. Strong liability with incomplete records usually moves at a moderate pace; waiting for the full medical packet often improves valuation accuracy. Disputed liability with strong records tends to move slower with moderate risk; prepare for a litigation posture to improve leverage. Disputed liability with weak records is typically slow and high risk; prioritize evidence development before negotiating.

Checklist: Settlement Readiness Review

- Crash report obtained and reviewed

- Medical treatment stabilized or prognosis documented

- Bills and records complete and organized

- Wage loss documentation verified

- Policy limits confirmed

Common Timeline Pitfalls

- Settling before reaching a stable medical outlook

- Missing statute of limitations deadlines

- Relying on verbal statements without records

- Ignoring comparative fault exposure

Medical Improvement and Settlement Timing

Settlement timing often depends on when medical treatment stabilizes. Many claims should wait until there is a clear prognosis or a provider indicates maximum medical improvement (MMI). This helps ensure that future care needs are documented and that settlement discussions reflect a complete medical picture.

Indicators of Medical Stabilization

- Discharge from therapy or a stable treatment plan

- Provider notes indicating expected future care

- Final billing summaries and treatment end dates

Additional Resources

For a systematic hiring process, review the hiring blueprint. For accident-type liability analysis, see intersection fault rules when available.

Non-Economic Loss Anchors

Non-economic damages are evaluated through medical records, treatment length, documented limitations, and consistency. Treatment gaps and inconsistent history reduce value. A short, conservative treatment path can still support a credible claim, but a complete record is critical.

Settle Now or Continue Treatment?

Ongoing pain with active treatment and incomplete records usually carries low to moderate risk in waiting; delaying may improve valuation accuracy. Symptoms resolved with complete records carries low risk in waiting; settling now is often efficient. Disputed causation with mixed records has moderate risk; additional diagnostics may help. Low and clear limits with complete records have low risk; early settlement may be prudent. Possible future care with incomplete records carries high risk; wait for prognosis support.

Common Valuation Errors to Avoid

- Settling before obtaining a stable medical outlook.

- Failing to document missed work or reduced duties.

- Relying on verbal injury descriptions without records.

- Overlooking comparative fault evidence in the report.

- Ignoring policy limit ceilings in negotiation strategy.

Internal Navigation: Related Car Accident Guides

- For a hiring framework, see the guide on choosing a car accident lawyer in 2026.

- For claim timing detail, review the car accident claim timeline breakdown.

- For property-only cases, use the property damage claim roadmap.

- For uninsured scenarios, read uninsured motorist claim steps.

- Return to the car accidents hub page for the full category.

- For process rules, reference the legal process topic hub.

Source Box (Official .gov References)

- National Highway Traffic Safety Administration (NHTSA): https://www.nhtsa.gov

- U.S. Courts Rules and Procedures: https://www.uscourts.gov/rules-policies/current-rules-practice-procedure

- Federal Motor Carrier Safety Administration (crash data and safety): https://www.fmcsa.dot.gov

Related Resources

For broader context, review the Car Accidents hub.

Related Guides

- Auto Accident Lawyer: What They Do and When You Need One

- Average Car Accident Settlement in the U.S.

- Car Accident Attorney Near Me: Questions to Ask Before You Sign

Pillar guide: Car Accident Lawyer: How to Choose the Right One (2026)

Helpful Tool

Use the Car Accident Settlement Calculator Google Sheets to organize documentation, expenses, and insurance claim records while applying this guide.

More Car Accidents Guides

Car Accident Claim Timeline

A complete timeline of a car accident claim, from immediate steps and evidence preservation to settlement or lawsuit milestones. Read our comprehensive and e...

Car Accident Lawyer: Settlement Guide & Injury Claim Timeline

Car Accident Lawyer settlement guide covering U.S. liability, evidence, insurance, damages, and injury claim timeline strategy. Read our comprehensive and ex...

Rental Car Accident Lawyer Guide

A guide to rental car accident claims, including liability layers, insurance coverage options, and evidence requirements. Read our comprehensive and expert l...

Left-Turn Accident Fault

A legal guide to left-turn accident fault, covering right-of-way rules, evidence priorities, and liability analysis for intersection crashes. Read our compre...

Uninsured Motorist Claim After a Car Accident

A step-by-step guide to uninsured motorist (UM) claims after a car accident, including coverage rules, evidence, and timing. Read our comprehensive and exper...

Rear-End Collision Settlement

A guide to rear-end collision settlement value, including liability assumptions, evidence strength, and damage documentation. Read our comprehensive and expe...

Related Documentation Tools

View all toolsThese free spreadsheets help organize evidence, deadlines, and claim documentation for this topic.

Car Accident Settlement Calculator Google Sheets

Estimate negotiable case value and keep damages evidence aligned with Settlement Calculator and Economic Damages before you share records with an insurer or attorney.

Car Accident Checklist Google Sheets

Build a timestamped evidence file that keeps facts consistent with Accident Overview and Driver Information before you share records with an insurer or attorney.

Car Accident Police Report Tracker Google Sheets

Build a timestamped evidence file that keeps facts consistent with Accident Overview and Police Report Log before you share records with an insurer or attorney.

Insurance Claim Tracker Google Sheets

Estimate negotiable case value and keep damages evidence aligned with Claim Overview and Claim Timeline before you share records with an insurer or attorney.