Summary

A legal guide to car accidents involving uninsured drivers, including coverage options, penalties, and claim strategies. Read our comprehensive and expert le...

Quick Legal Answer: What this guide covers

A legal guide to car accidents involving uninsured drivers, including coverage options, penalties, and claim strategies. Read our comprehensive and expert le...

Quick Legal Answer: Core legal focus

This guide focuses on car accident with no insurance within car accident guides and the evidence, timelines, and standards typically evaluated under U.S. law.

Quick Legal Answer: When to verify with counsel

Because statutes and rules vary by state, confirm the specifics for your jurisdiction with a qualified attorney or official government resources.

Key Takeaways

- Understand the core rules and evidence standards tied to car accident with no insurance.

- Track deadlines and procedural steps that shape recovery options.

- Document medical records, liability proof, and insurance communications early.

- Compare settlement posture with litigation risk based on the case record.

Car Accident With No Insurance

Car accidents involving uninsured drivers raise serious legal and financial risks. This guide on car accident with no insurance issues explains what happens when you lack coverage, what claim options exist when the other driver is uninsured, and how state rules shape recovery. Planning should account for uninsured driver penalties, available UM coverage, and the realistic ceiling set by policy limits. A credible strategy also ties the car accident settlement to the auto accident claim record, collision liability, and documented personal injury damages. It should flag insurance bad faith, document a pain and suffering claim, and track medical bills recovery and lost wages claim. Settlement posture depends on comparative fault rules and the strength of the demand package.

This overview explains how car accident with no insurance considerations shape evidence, liability, and recovery planning.

State laws vary widely. Some states impose no-pay, no-play rules that restrict recovery for uninsured drivers, while others allow recovery but still apply uninsured driver penalties such as license suspension, vehicle impoundment, or SR-22 filing requirements. Understanding your state’s rules is critical to planning next steps and avoiding avoidable mistakes.

Definitions and Key Concepts

Key terms below appear throughout claims and state statutes.

- Uninsured driver: A driver with no active insurance policy, which can create civil liability and penalties.

- UM coverage: Uninsured motorist coverage that may pay when the other driver has no insurance.

- UIM coverage: Underinsured motorist coverage that may apply when the other driver’s limits are too low.

- No-pay, no-play rules: State restrictions that can reduce or bar certain damages for uninsured drivers.

- SR-22: Proof of financial responsibility often required after violations.

- Subrogation: An insurer reimbursement claim that can reduce net recovery.

Scenario 1: You Are Uninsured and Not at Fault

Potential Consequences

- State penalties for driving without insurance, including uninsured driver penalties

- Possible restrictions on non-economic damages such as pain and suffering damages in some states

- Requirement to file proof of insurance (SR-22)

Claim Options

- File a liability claim against the at-fault driver

- Use health insurance for medical treatment, while accounting for a potential health insurance lien

- Consider a personal injury lawsuit if permitted by state law and supported by evidence

Scenario 2: The Other Driver Is Uninsured

Primary Options

- Use your UM coverage or uninsured motorist coverage if available and policy conditions are met

- Use collision coverage for property damage if you carry it

- Consider a lawsuit against the at-fault driver, recognizing collection risks and asset limits

Scenario 3: Both Drivers Are Uninsured

When both parties lack insurance, recovery options are limited. Claims may require direct negotiation or civil litigation, but collection can be difficult without assets. Evidence still matters because it determines liability and the value of damages.

Step-by-Step: What to Do After an Uninsured Crash

Step 1: Report the Crash

File a police report and document the scene. Reporting is often required by law and supports any later claim options.

Step 2: Seek Medical Care

Medical records are essential for any claim, even if coverage is unclear. Early care also protects your health and provides objective documentation.

Step 3: Identify Coverage Options

Check for UM/UIM coverage, collision coverage, or MedPay/PIP benefits. These coverages can apply even if the other driver has no insurance.

Step 4: Document All Damages

Collect medical records, wage loss documentation, and repair estimates.

Step 5: Evaluate State-Specific Restrictions

Determine whether your state limits recovery for uninsured drivers.

Evidence Checklist

- Police report and citation data

- Photos of the scene and vehicle damage

- Medical records and bills

- Wage loss verification

- Insurance policy declarations

Claim Paths Without Insurance

- You are uninsured and the other driver is insured: A liability claim may be available with a police report and medical records.

- You are insured and the other driver is uninsured: A UM claim may apply with a police report and coverage proof.

- Both drivers are uninsured: A civil claim is possible but often limited by asset availability and collection risk.

- Property damage only: Collision coverage may apply with repair estimates and photos.

No-Pay, No-Play Rules

Some states restrict uninsured drivers from recovering non-economic damages such as pain and suffering. These rules vary and may not apply to all cases, and exceptions can exist depending on state statutes.

Questions to Ask About State Rules

- Does my state bar non-economic damages for uninsured drivers?

- Are there exceptions for medical emergencies or other circumstances?

- Does comparative fault change the restriction?

Penalties for Driving Without Insurance

Penalties can include fines, license suspension, vehicle impoundment, and SR-22 requirements. These penalties are separate from any civil claim and depend on state law.

Evidence and Documentation Priorities

Even if you are uninsured, evidence still determines liability and damages. A well-documented file improves claim outcomes, supports settlement negotiations, and reduces disputes.

Documentation Checklist

- Crash report and citation data

- Photos of vehicle damage and scene

- Medical records and bills

- Wage loss documentation

- Insurance communications and policy declarations

Settlement and Negotiation Considerations

Uninsured status can complicate negotiations. If the other driver’s insurer is involved, they may raise state law restrictions or comparative fault arguments. Know your state’s rules before negotiating settlement terms.

Negotiation Tips

- Keep communication documented in writing

- Provide complete evidence packets

- Avoid speculative statements about fault

Step-by-Step: If You Are Uninsured and At Fault

- Report the crash and cooperate with law enforcement.

- Notify the other driver’s insurer if contacted.

- Document damages and injuries of all parties.

- Evaluate whether payment plans or settlement options are available.

- Obtain insurance promptly to avoid ongoing penalties.

Step-by-Step: If You Are Uninsured and Not at Fault

- File a claim against the at-fault driver’s insurer.

- Provide the crash report and medical records.

- Document wage loss and out-of-pocket expenses.

- Review your state’s recovery restrictions for uninsured drivers.

- Consider legal guidance if coverage disputes arise.

Checklist: Uninsured Driver Claim Readiness

- Police report obtained

- Insurance coverage confirmed

- Medical records organized

- State law restrictions reviewed

- All damages documented

Internal Navigation: Related Car Accident Guides

- For UM claim steps, see the uninsured motorist guide.

- For hit-and-run issues, read the hit-and-run guide.

- For claim timing, see the claim timeline guide.

- For settlement context, read average settlement analysis.

- Return to the car accidents hub.

Source Box (Official .gov References)

- National Highway Traffic Safety Administration: https://www.nhtsa.gov

- U.S. Department of Transportation: https://www.transportation.gov

- USA.gov insurance resources: https://www.usa.gov/insurance

- U.S. Courts: https://www.uscourts.gov

Related Resources

For broader context, review the Car Accidents hub.

Related Guides

- Auto Accident Lawyer: What They Do and When You Need One

- Average Car Accident Settlement in the U.S.

- Car Accident Attorney Near Me: Questions to Ask Before You Sign

Pillar guide: Car Accident Lawyer: How to Choose the Right One (2026)

Helpful Tool

Use the Car Accident Case Preparation Checklist Google Sheets to organize documentation, expenses, and insurance claim records while applying this guide.

More Car Accidents Guides

Car Accident Lawyer: Settlement Guide & Injury Claim Timeline

Car Accident Lawyer settlement guide covering U.S. liability, evidence, insurance, damages, and injury claim timeline strategy. Read our comprehensive and ex...

Rental Car Accident Lawyer Guide

A guide to rental car accident claims, including liability layers, insurance coverage options, and evidence requirements. Read our comprehensive and expert l...

Left-Turn Accident Fault

A legal guide to left-turn accident fault, covering right-of-way rules, evidence priorities, and liability analysis for intersection crashes. Read our compre...

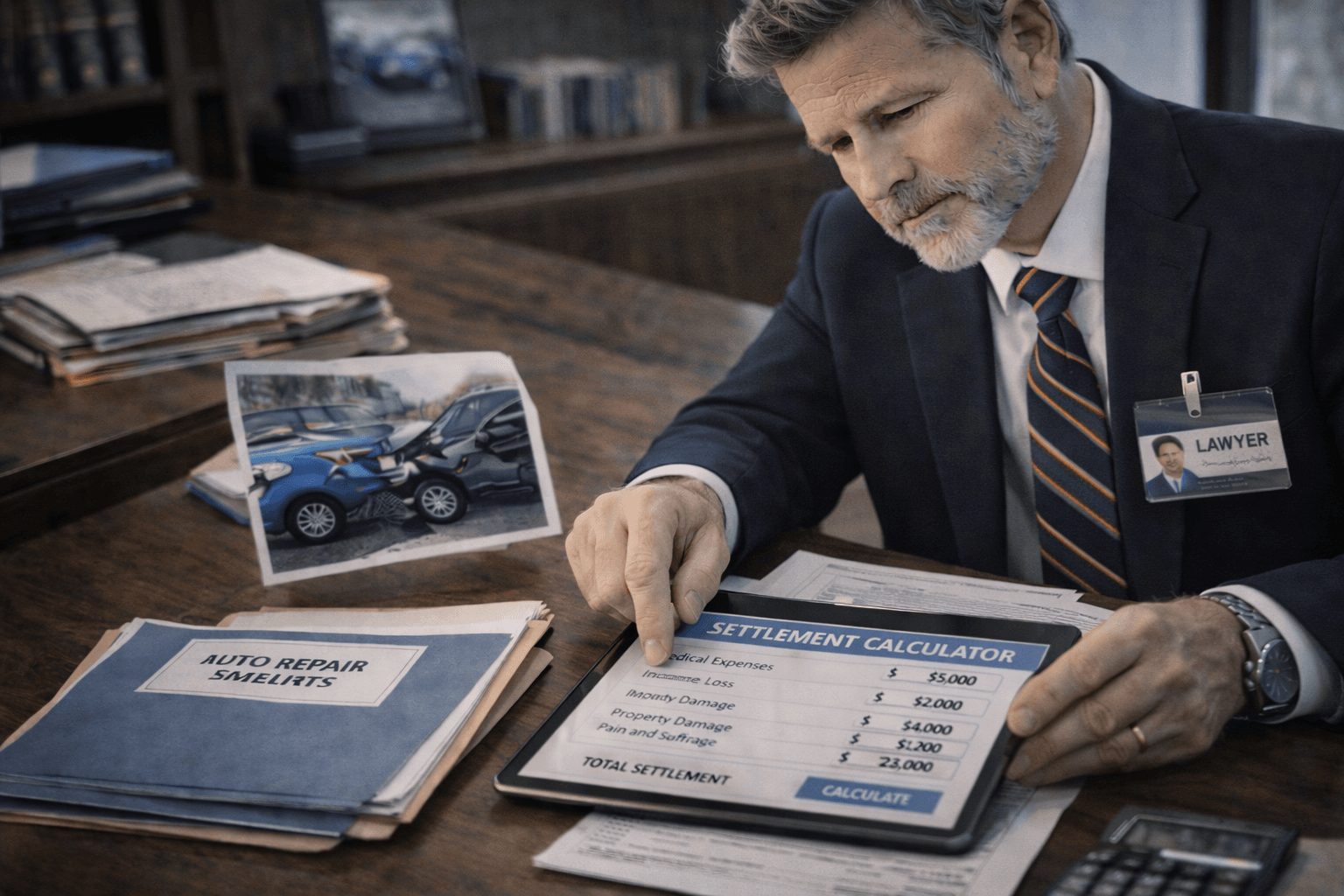

Car Accident Settlement Calculator

A legal-safe settlement calculator framework that explains the inputs, evidence requirements, and limitations of estimating car accident value. Read our comp...

Uninsured Motorist Claim After a Car Accident

A step-by-step guide to uninsured motorist (UM) claims after a car accident, including coverage rules, evidence, and timing. Read our comprehensive and exper...

Rear-End Collision Settlement

A guide to rear-end collision settlement value, including liability assumptions, evidence strength, and damage documentation. Read our comprehensive and expe...

Related Documentation Tools

View all toolsThese free spreadsheets help organize evidence, deadlines, and claim documentation for this topic.

Car Accident Settlement Calculator Google Sheets

Estimate negotiable case value and keep damages evidence aligned with Settlement Calculator and Economic Damages before you share records with an insurer or attorney.

Car Accident Checklist Google Sheets

Build a timestamped evidence file that keeps facts consistent with Accident Overview and Driver Information before you share records with an insurer or attorney.

Car Accident Police Report Tracker Google Sheets

Build a timestamped evidence file that keeps facts consistent with Accident Overview and Police Report Log before you share records with an insurer or attorney.

Insurance Claim Tracker Google Sheets

Estimate negotiable case value and keep damages evidence aligned with Claim Overview and Claim Timeline before you share records with an insurer or attorney.