Summary

A complete guide to property damage claims after a car accident, including repair estimates, total loss valuation, and documentation. Read our comprehensive ...

Quick Legal Answer: What this guide covers

A complete guide to property damage claims after a car accident, including repair estimates, total loss valuation, and documentation. Read our comprehensive ...

Quick Legal Answer: Core legal focus

This guide focuses on property damage claim car accident within car accident guides and the evidence, timelines, and standards typically evaluated under U.S. law.

Quick Legal Answer: When to verify with counsel

Because statutes and rules vary by state, confirm the specifics for your jurisdiction with a qualified attorney or official government resources.

Key Takeaways

- Understand the core rules and evidence standards tied to property damage claim car accident.

- Track deadlines and procedural steps that shape recovery options.

- Document medical records, liability proof, and insurance communications early.

- Compare settlement posture with litigation risk based on the case record.

Property Damage Claim After a Car Accident

property damage claim car accident

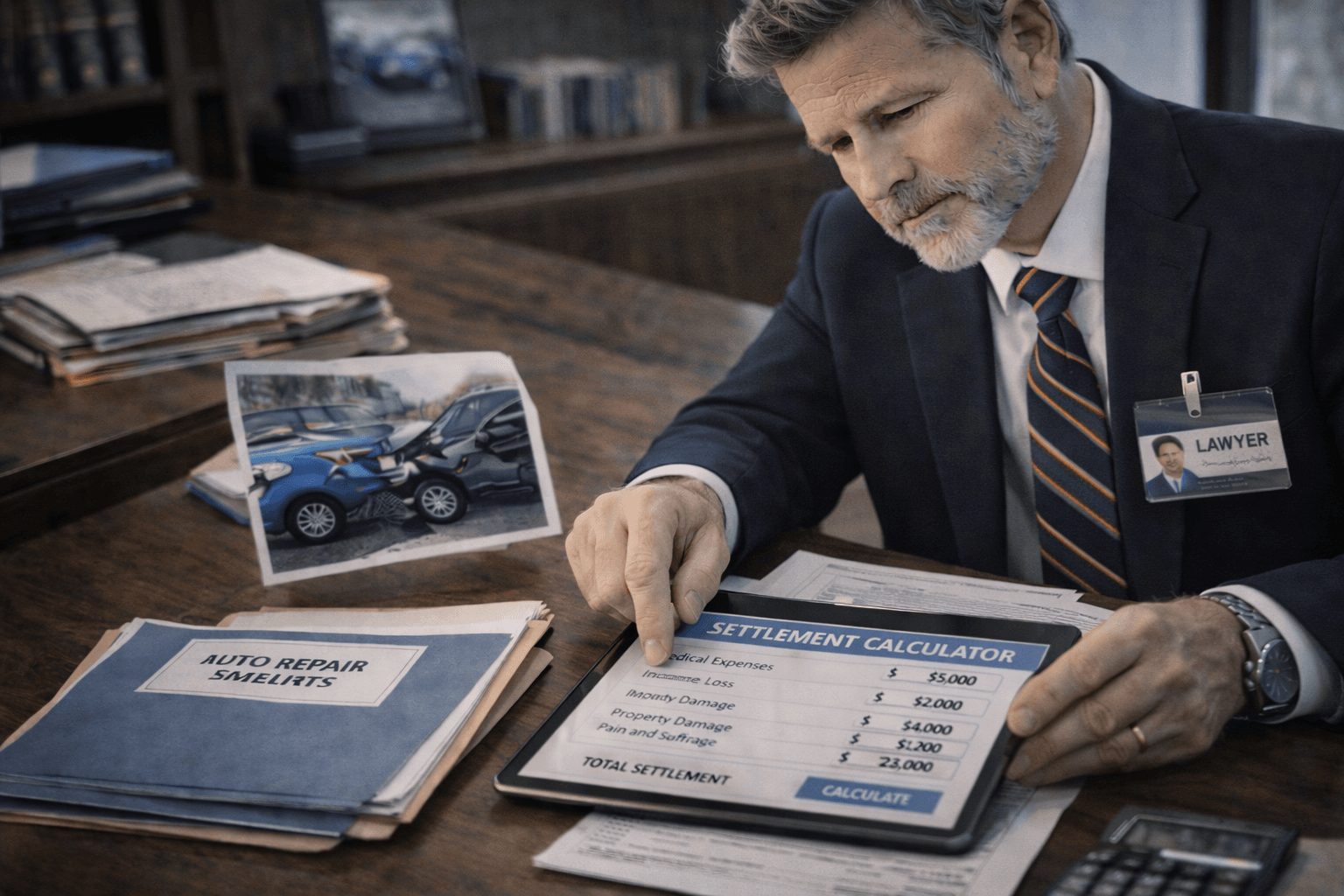

Property damage claims focus on repairing or replacing a vehicle after a crash. This guide explains how total loss valuation, a credible repair estimate, and diminished value evidence shape outcomes. A complete file should connect the car accident settlement range to the auto accident claim timeline, collision liability, and full personal injury damages profile. It should also flag insurance bad faith, document a pain and suffering claim, preserve medical bills recovery and lost wages claim proof, apply comparative fault rules, and support a clear demand package within policy limits.

This overview explains how property damage claim car accident considerations shape evidence, liability, and recovery planning.

Property damage claims are separate from injury claims, but they often run in parallel. Keeping the property damage file organized helps prevent delays and disputes, especially when a vehicle is declared a total loss.

Definitions Used in Property Damage Claims

Definition Table

The Term refers to repair estimate. Practical Meaning: Projected cost to fix vehicle. Why It Matters: Determines repair vs total loss. The Term refers to total loss. Practical Meaning: Repair cost exceeds vehicle value. Why It Matters: Triggers valuation process. The Term refers to actual cash value (ACV). Practical Meaning: Market value before crash. Why It Matters: Basis for total loss payment. The Term refers to diminished value. Practical Meaning: Reduced resale value after repair. Why It Matters: May be recoverable in some states. The Term refers to loss of use. Practical Meaning: Compensation for rental or downtime. Why It Matters: Often tied to rental coverage.

Step-by-Step Property Damage Claim Process

Step 1: Report the Crash

Notify the insurer and open a property damage claim. Provide the crash report number if available.

Step 2: Document the Damage

Take photos of all damage and keep repair estimates or towing invoices.

Step 3: Vehicle Inspection

Insurers often inspect the vehicle or request a digital photo estimate. If damage is hidden, supplemental estimates may be required.

Step 4: Repair or Total Loss Decision

If repair costs exceed a percentage of the vehicle’s value, the insurer may declare it a total loss.

Step 5: Settlement and Payment

Repair claims pay the shop or the vehicle owner. Total loss claims pay the vehicle’s actual cash value minus any deductible.

Evidence Checklist for Property Damage

- Photos of damage from multiple angles

- Repair estimates and supplements

- Towing and storage receipts

- Rental car invoices (if applicable)

- Vehicle records showing condition and upgrades

Total Loss Valuation Explained

Insurers use valuation reports based on comparable vehicles. Factors include mileage, prior condition, options, and local market pricing.

Total Loss Checklist

- Review the valuation report for accuracy

- Confirm mileage and condition ratings

- Provide receipts for recent upgrades

- Compare similar vehicles in your area

Diminished Value Claims

What It Is

Diminished value is the loss in resale value after repairs. Some states allow these claims, while others limit them.

Evidence for Diminished Value

- Pre-accident valuation

- Repair records showing structural work

- Post-repair appraisal

- Comparable vehicle sales data

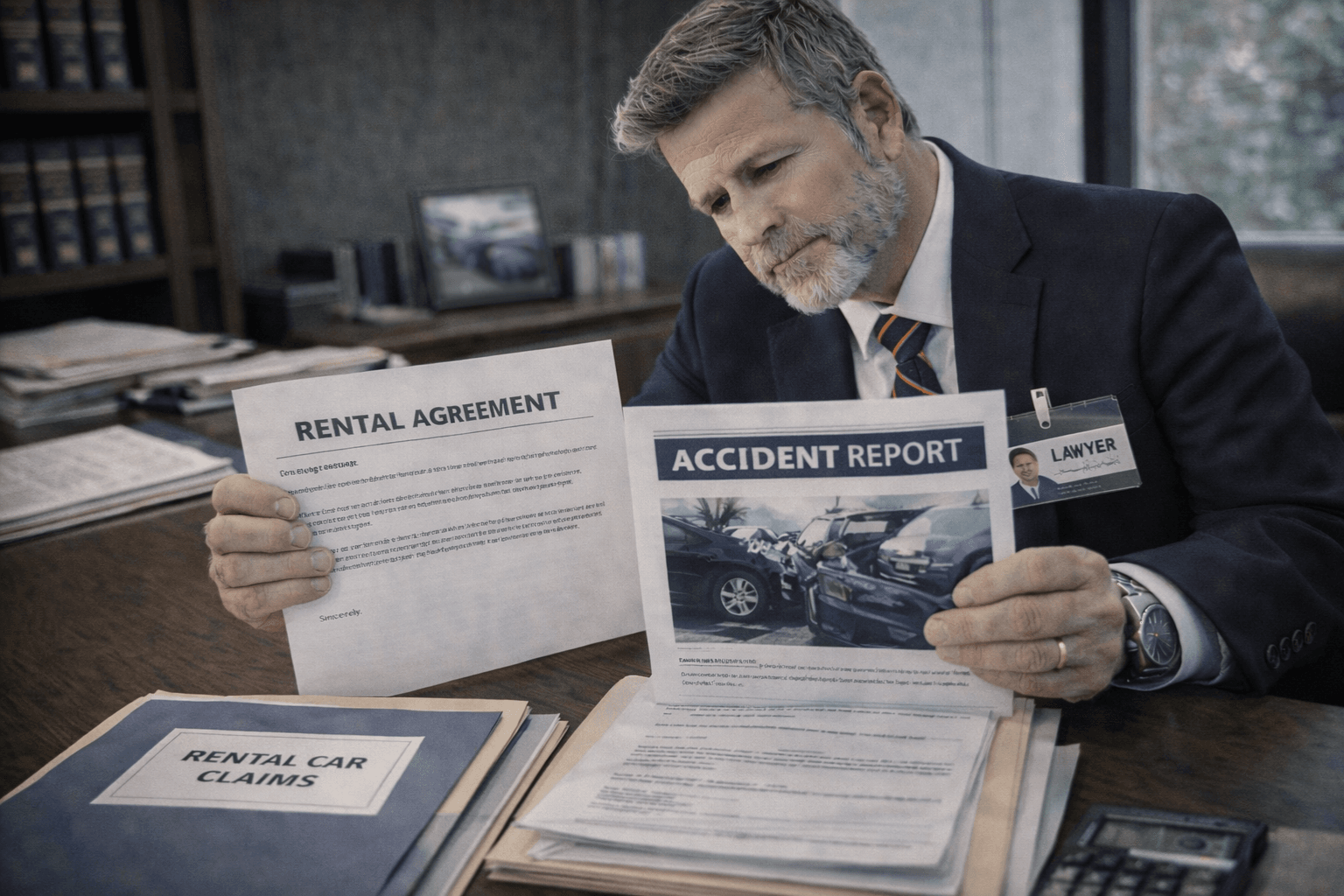

Loss of Use and Rental Reimbursement

Loss of use refers to the time your vehicle is unavailable. Some insurers provide rental reimbursement or direct compensation. Documentation is required, including rental receipts or proof of alternative transportation costs.

Loss of Use Checklist

- Rental agreements and receipts

- Dates of repair or total loss processing

- Repair shop timelines or parts delays

Repair Shop Choice and State Rules

Many states allow consumers to choose their repair shop. Insurers may recommend preferred shops, but you generally have a right to select a qualified provider.

Shop Selection Tips

- Obtain at least one independent estimate

- Confirm warranty terms on repair work

- Keep copies of all repair invoices

Supplemental Damage Claims

Hidden damage may be discovered after repairs begin. Supplemental estimates should be documented and approved by the insurer.

Supplemental Estimate Checklist

- Photos of newly discovered damage

- Updated estimate from the repair shop

- Written insurer approval

Decision Table: Repair vs Total Loss

The Factor refers to repair cost vs value. Repair: Lower. Total Loss: Higher. Why It Matters: Determines insurer decision. The Factor refers to structural damage. Repair: Limited. Total Loss: Extensive. Why It Matters: Safety and cost issues. The Factor refers to availability of parts. Repair: Readily available. Total Loss: Delayed or scarce. Why It Matters: Affects timeline. The Factor refers to vehicle age. Repair: Newer. Total Loss: Older. Why It Matters: Impacts ACV.

Step-by-Step: Disputing a Total Loss Value

Request the valuation report and review details. Gather comparable listings with similar mileage and condition. Provide receipts for upgrades or recent maintenance. Submit a written dispute with supporting documentation.

Property Damage Timeline

Typical Timeline Ranges

- Inspection and estimate: 1-2 weeks

- Repairs with parts available: 2-6 weeks

- Total loss valuation: 2-4 weeks

- Disputes or supplements: longer depending on documentation

Checklist: Property Damage Claim Readiness

- Damage photos and repair estimate saved

- Towing and storage receipts organized

- Rental invoices tracked

- Vehicle maintenance records available

- Valuation report reviewed for accuracy

Internal Navigation: Related Car Accident Guides

- For claim timing, see the claim timeline guide.

- For settlement context, read average settlement analysis.

- For report documentation, use the police report guide.

- For rear-end liability, see rear-end fault and evidence.

- Return to the car accidents hub.

Source Box (Official .gov References)

- National Highway Traffic Safety Administration: https://www.nhtsa.gov

- U.S. Department of Transportation: https://www.transportation.gov

- USA.gov insurance resources: https://www.usa.gov/insurance

- U.S. Courts: https://www.uscourts.gov

Related Resources

For broader context, review the Car Accidents hub.

Related Guides

- Auto Accident Lawyer: What They Do and When You Need One

- Average Car Accident Settlement in the U.S.

- Car Accident Attorney Near Me: Questions to Ask Before You Sign

Pillar guide: Car Accident Lawyer: How to Choose the Right One (2026)

Helpful Tool

Use the Car Accident Lost Wages Calculator Google Sheets to organize documentation, expenses, and insurance claim records while applying this guide.

More Car Accidents Guides

Car Accident Settlement Calculator

A legal-safe settlement calculator framework that explains the inputs, evidence requirements, and limitations of estimating car accident value. Read our comp...

Car Accident Lawyer: Settlement Guide & Injury Claim Timeline

Car Accident Lawyer settlement guide covering U.S. liability, evidence, insurance, damages, and injury claim timeline strategy. Read our comprehensive and ex...

Rental Car Accident Lawyer Guide

A guide to rental car accident claims, including liability layers, insurance coverage options, and evidence requirements. Read our comprehensive and expert l...

Intersection Accident Fault

A legal guide to intersection accident fault, including right-of-way rules, evidence collection, and liability analysis. Read our comprehensive and expert le...

Uninsured Motorist Claim After a Car Accident

A step-by-step guide to uninsured motorist (UM) claims after a car accident, including coverage rules, evidence, and timing. Read our comprehensive and exper...

Rear-End Collision Settlement

A guide to rear-end collision settlement value, including liability assumptions, evidence strength, and damage documentation. Read our comprehensive and expe...

Related Documentation Tools

View all toolsThese free spreadsheets help organize evidence, deadlines, and claim documentation for this topic.

Car Accident Settlement Calculator Google Sheets

Estimate negotiable case value and keep damages evidence aligned with Settlement Calculator and Economic Damages before you share records with an insurer or attorney.

Car Accident Checklist Google Sheets

Build a timestamped evidence file that keeps facts consistent with Accident Overview and Driver Information before you share records with an insurer or attorney.

Car Accident Police Report Tracker Google Sheets

Build a timestamped evidence file that keeps facts consistent with Accident Overview and Police Report Log before you share records with an insurer or attorney.

Insurance Claim Tracker Google Sheets

Estimate negotiable case value and keep damages evidence aligned with Claim Overview and Claim Timeline before you share records with an insurer or attorney.